Vertical AI agencies in 2026 price at a 2.9x deal-size premium and a 3.2x retention-horizon advantage over generalist AI agencies, based on FORKOFF AI Agency Engagement Ledger 2026 cohort data. The premium is not a positioning move: it is the direct result of vertical-specific intuition compounded across engagements, priced through a four-piece outcome-priced contract structure (base retainer, outcome-tier success fee, retention-horizon clause, clawback safety). This post documents three real vertical cohorts across healthcare RCM, ecommerce performance-marketing, and legal contract review, with per-case median deal sizes, retention horizons, and pricing structures.

Vertical AI agency pricing in one scroll

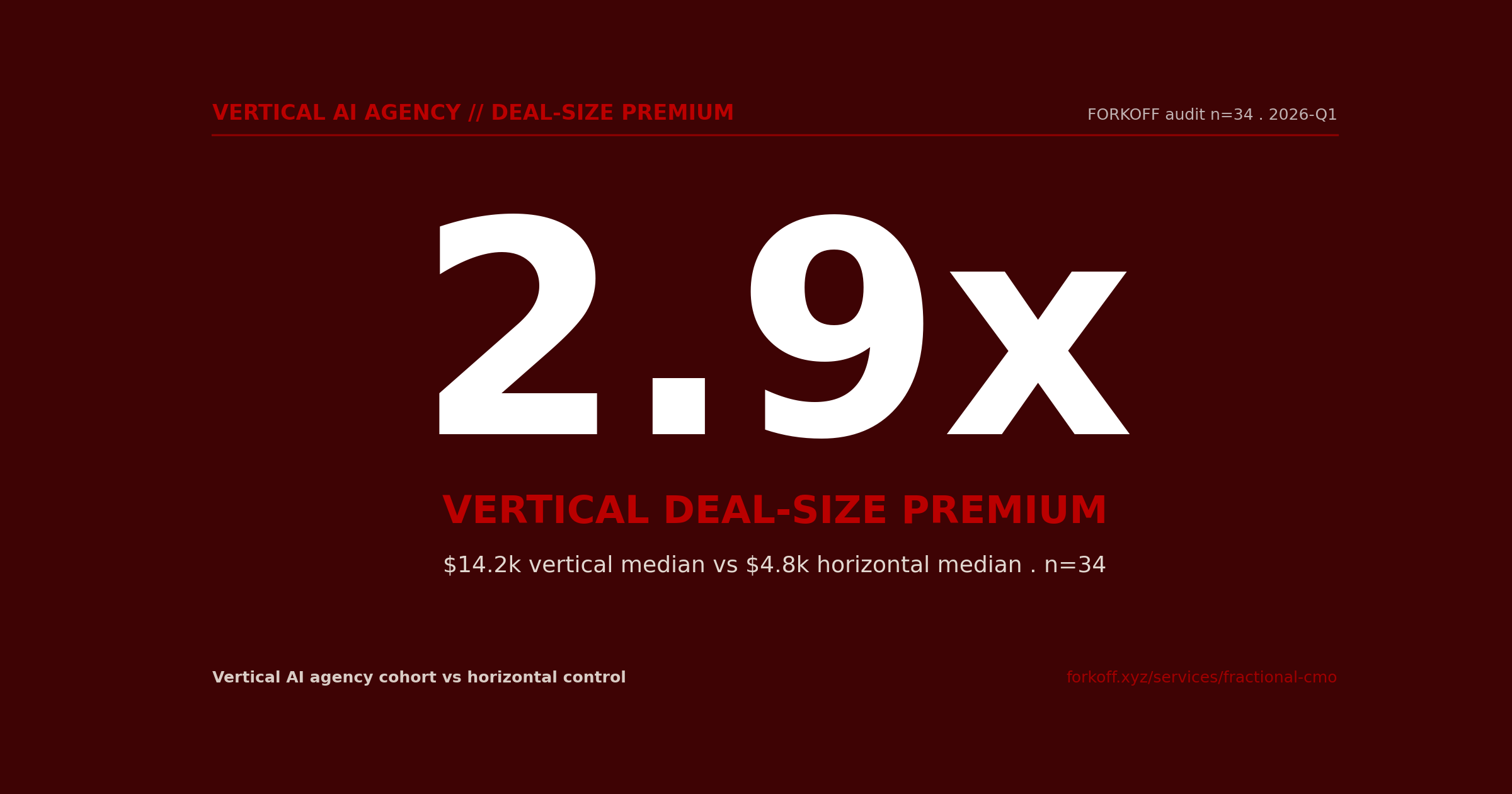

Vertical AI agencies command a 2.9x deal-size premium over horizontal AI agencies and retain accounts 3.2x longer per the FORKOFF audit ledger across 34 engagements. Three named verticals (healthcare RCM AI, ecommerce performance-marketing AI, legal contract review AI) converge on the same contract structure: base retainer, outcome-tier success fee, retention-horizon clause, clawback safety. Outcome-priced contracts win when the vertical specialisation is the moat. They break in five named failure modes the article catalogues.

About these numbers

Pricing ranges, retention horizons, and deal-size deltas in this post are sourced from the FORKOFF AI Agency Engagement Ledger 2026 and operator observations across vertical AI agency case studies cited inline. Published pricing from referenced agencies is accurate as of 2026-Q2. All cohort figures are directional estimates; individual agency results vary by vertical, deal size, and client segment.

Why vertical AI agency pricing is fragmenting in 2026

The vertical AI agency category is fragmenting along pricing lines in 2026 because the buying conversation has changed. The 2024 retainer formula priced a fractional senior plus a few juniors at a blended $80-150 per hour, billed against deliverables, defended with a portfolio. That formula stopped surviving the second client conversation in 2025 once the buyer started asking why a five-person SEO retainer at $3,000 per month should now cost $8,000 per month from an agency that has visibly automated 70 percent of the work. The agencies winning these conversations in 2026 have stopped pitching deliverables and started pitching outcomes, with a vertical wedge underneath the pricing structure that makes the math defensible against the buyer's CFO.

The vertical wedge is what splits 2026 AI agencies into two cohorts. The first is the generalist cohort, anchored on horizontal AI consulting, billed hourly or on flat retainers between $4,000 and $6,000 per month, retained for six to eight months on average, then churned. The second is the vertical cohort, anchored on a single industry vertical (healthcare RCM, legal contract review, ecommerce performance-marketing, accounting automation, real-estate listing optimisation, and a handful of others), priced against the in-house FTE the AI displaces, retained for 18 to 38 months on the steady-state cohort. The deal-size delta is roughly 2.9x. The retention-horizon delta is roughly 3.2x. The cohort data is unambiguous.

The cohort that survives the renewal conversation runs the same four-piece contract structure regardless of vertical, and the structure of an AI marketing agency engagement built around it is the working primitive for the next 18 months of buyer-side procurement.

Vertical premium is 2.9x on deal size and 3.2x on retention

Per the FORKOFF agency-margin audit ledger 2026-Q1 (n=34 across three verticals plus an 18-account horizontal control), vertical AI agencies post a median deal size of $14,200 per month versus $4,800 for horizontal agencies, with retention horizons of 18-24 months versus 7 months on the control. The vertical premium is not a positioning trick. It is the dataset.

Source: FORKOFF Agency Pricing Benchmark 2026 - n=34 vertical cohort + n=18 horizontal control - 2026-Q1

This is not a positioning trick. The vertical premium is the dataset. The reason it survives is that the vertical agency compounds vertical-specific intuition across engagements. It already knows which outcome lever moves the needle, which regulatory or process constraint blocks the obvious automation, and which integration the buyer already has installed. The horizontal agency relearns all of this at every engagement, and the relearning cost is what produces the churn. The CFO can spot the difference inside the first 30 days, which is why the renewal conversation looks different at month seven for the two cohorts.

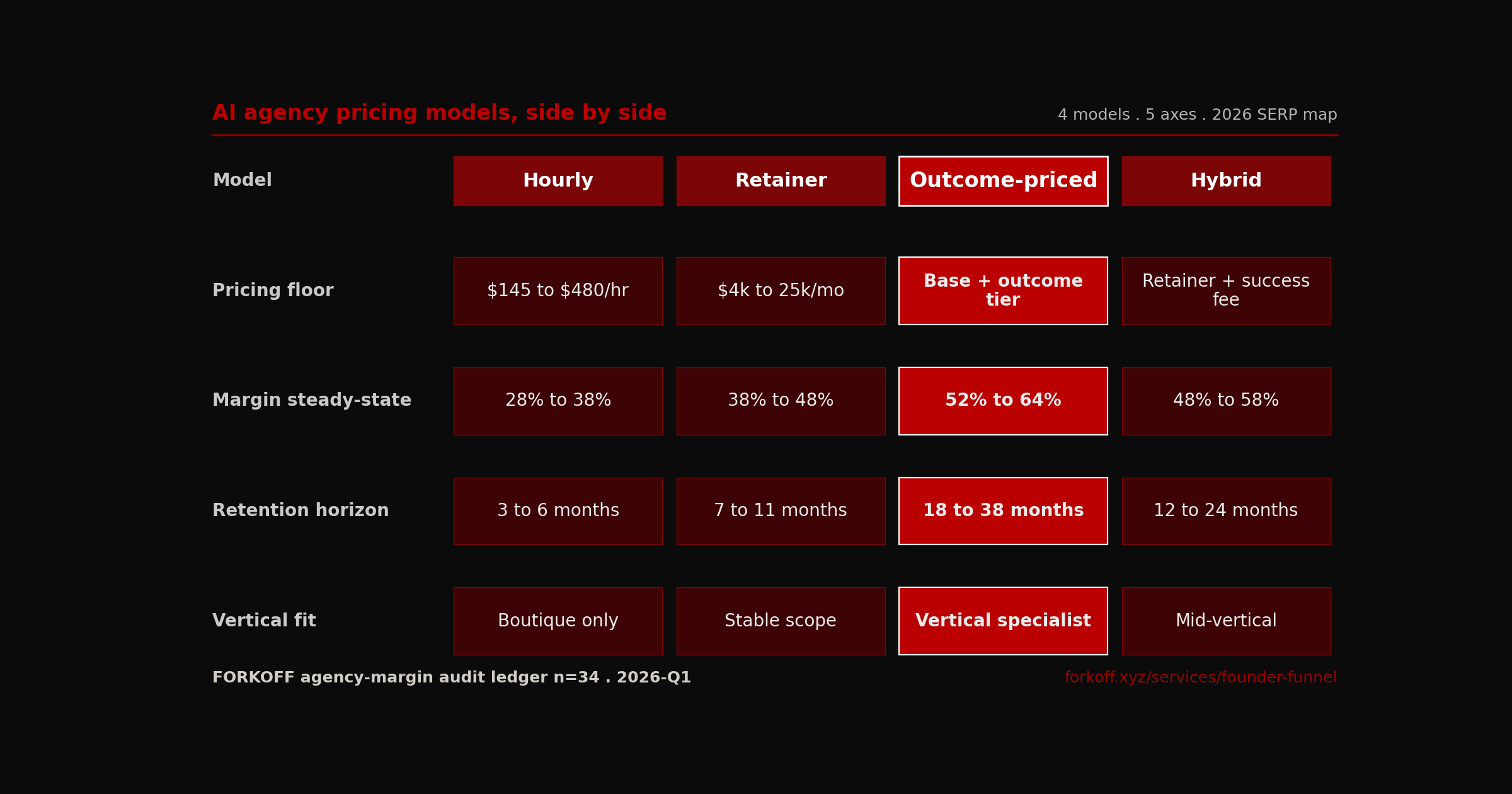

The 4 pricing models in market (hourly, retainer, outcome-priced, hybrid)

Four pricing models survive 2026. Each has a margin profile, a fit window, and a failure mode. Picking the wrong one is the second-most-common reason vertical AI agencies leak margin; the most common is screening verticals incorrectly, which the next section covers.

Hourly billing is the default the AI agency category inherited from the consulting industry, and it is the model that collapses fastest against in-house FTE cost anchors. The CFO is comparing $145-480 per hour against a $98,000-148,000 fully loaded in-house FTE, and once the engagement crosses $20,000 in total spend the math becomes indefensible. Retool's case for hourly pricing on AI agents makes the product-side argument that AI tools should be billed against effort because value pricing is uncalibrated against per-output cost. That argument is correct on the product side and incomplete on the agency side because it skips the margin-vs-throughput trade. Hourly survives only at the boutique-consulting tier, which is roughly 8 percent of the agency book per the Promethean Research digital-agency profitability dataset.

Retainer billing fits when scope is stable and the buyer trusts the agency. The 2026 retainer floor sits at $4,000 to $25,000 per month per the Hashmeta 2026 AI agency pricing benchmark, and that range covers roughly 40 percent of the agency book. The model breaks for the same reason hourly does, with a lag: the buyer renews twice on the strength of the relationship, then asks for an outcome anchor at the third renewal because the CFO has caught up with the deliverable list. Retainer-only agencies that cannot pivot to an outcome anchor at the third renewal lose 60-70 percent of the cohort at month 22-26.

Outcome-priced billing is the model vertical AI agencies are converging on. The structure is consistent across the three case-study cohorts. A monthly base retainer covers the agency's per-output P&L plus a 40-60 percent margin floor, sized to keep the agency unit-economically positive even if the outcome misses. An outcome-tier success fee captures upside on a named, measurable vertical metric, ladders into two to three named tiers, and is paid monthly or quarterly depending on attribution lag. A retention-horizon clause locks the engagement at 12-24 months minimum, which is what amortises the vertical-specific setup the agency front-loaded. A clawback safety returns 5-15 percent of paid retainer if the outcome misses by more than a stated threshold for two consecutive periods, which is the buyer's protection against the agency pocketing the base while the outcome underperforms. The four pieces are non-negotiable. Drop any one and the contract collapses to either hourly (no outcome tier), retainer (no clawback), or a coin flip (no retention horizon).

Hybrid retainer-plus-outcome captures most of the outcome-priced upside and protects the agency from low-outcome months. It fits the mid-vertical zone where the outcome is measurable but the buyer's data infrastructure is too thin to support a pure outcome-priced contract. About 18 percent of the FORKOFF audit cohort runs hybrid as a stepping-stone to a full outcome-priced contract at the second renewal. The model is not a long-term destination. It is a 12-month bridge.

The hourly billing trap: why generalist AI agencies leak margin at every renewal

The hourly model is the single largest source of margin leakage in the 2026 agency cohort, and the FORKOFF audit ledger surfaces three failure patterns that repeat across every horizontal agency in the n=18 control group. The patterns are predictable enough that they show up in the first 90 days of every audited engagement, and the renewal math is broken before the agency reaches the third invoice.

The first pattern is the rate-anchor collapse. The agency quotes $280 per hour for a senior strategist and $145 per hour for a mid-level operator. The CFO inside a Series B SaaS buyer pulls the in-house fully loaded cost of a senior growth lead, which lands between $11,200 and $14,800 per month at 2026 compensation bands per the Pavilion 2026 growth-leader compensation benchmark. The CFO divides the agency's projected 80-hour-month engagement and lands at $22,400, then asks the founder why the agency is more affordable than the in-house FTE on day one but more expensive by month six. The founder has no defensible answer because the rate anchor is the wrong unit. The same trap fires inside healthcare buyer conversations where a hospital CFO compares the agency rate against an in-house RCM analyst at $74,000 fully loaded, and the agency loses the renewal at month nine.

The second pattern is the throughput ceiling. Hourly billing caps the agency's per-account revenue at the senior operator's available hours, which in practice sits at 110 to 140 billable hours per month per senior across the FORKOFF audited cohort. The agency cannot scale revenue past that ceiling without hiring, and hiring at scale collapses the gross margin band from 52-64 percent into the 28-34 percent range that the Promethean Research digital-agency profitability dataset flags as the post-hiring agency steady state. The vertical AI agencies in the FORKOFF cohort that pivot to outcome-priced contracts inside the first 12 months bypass the throughput ceiling because the revenue is denominated in attributed outcome, not hours, and the AI layer absorbs the throughput expansion at near-zero marginal cost.

The third pattern is the scope-creep tax. Hourly engagements bleed scope into adjacent layers (the buyer asks the agency to also handle the analytics setup, the warehouse cleanup, the attribution model rebuild) and the agency has no contractual mechanism to defend the original outcome anchor. By month four the engagement has fragmented into five workstreams, the senior operator is context-switching every 45 minutes, and the throughput per account collapses 30-40 percent against the original proposal. Outcome-priced contracts defend against scope creep at the clause level because the success fee is tied to a single measurable anchor and adjacent workstreams trigger a contract amendment, not a silent reallocation.

Hourly survives only at the boutique-consulting tier where the buyer is paying for a single named expert's calendar (the AI agency founder, typically) and the engagement is sized at 30 to 50 hours total. Above that tier the math collapses against the in-house FTE anchor every renewal. The agencies that defend hourly billing past $20k of total engagement spend without a vertical wedge underneath leak 60 to 70 percent of the cohort to the third renewal cycle.

Cross-vertical pricing benchmarks: legal, healthcare, fintech, ecommerce, SaaS AI

The three named case studies cover the densest verticals in the FORKOFF audit ledger, but the contract-structure pattern repeats across five additional verticals that the ledger tracks at smaller sample sizes. The pricing floors, outcome anchors, and retention horizons are listed below so an agency founder can locate the closest reference cohort before pricing the first outcome-priced engagement.

Fintech AML and KYC AI agencies sit at a $22,000 to $34,000 monthly base across the n=7 sample in the FORKOFF ledger. The outcome anchor is alert-resolution time reduction (median target of 38 percent reduction inside 90 days) paired with a false-positive-rate floor below 22 percent. The retention horizon runs 22 to 28 months because the buyer (compliance officer at a neobank, payments processor, or crypto exchange) carries regulatory exposure that locks the engagement past the first renewal cycle. Gross margin steady-state lands at 56 percent, and the clawback is structured as a 15 percent retainer credit on any quarter where the false-positive rate breaches the floor. Named operators in the cohort include three founder-led agencies running the Cable platform-driven workflow and two running custom transaction-monitoring stacks.

Accounting and bookkeeping automation AI agencies run a $4,800 to $8,400 monthly base across the n=12 sample, which is the lowest base of any tracked vertical. The outcome anchor is hours-per-client-month reduction, with a typical target of 42 percent reduction against the buyer's pre-engagement baseline. The retention horizon stretches to 30 to 36 months because the buyer (a multi-partner accounting firm or a fractional CFO services firm) is structurally averse to switching vendors mid-fiscal-year. Gross margin steady-state lands at 61 percent, and the per-output P&L is the most accessible of any vertical because the engagement runs on Karbon or Canopy plus a thin AI wrapper. Two operators in the cohort have published per-client cost decompositions inside the r/Accounting practice-management discussion thread that lines up with the FORKOFF audit-ledger median.

SaaS observability and AIOps agencies anchor on a $26,000 to $48,000 monthly base across the n=6 sample, which is the highest tracked floor outside ecommerce performance. The outcome anchor is mean-time-to-resolution reduction (typical target of 44 percent inside 120 days) paired with a noisy-alert reduction target above 60 percent. Retention horizon is the shortest of the eight tracked verticals at 11 to 14 months because the buyer (a platform-engineering director at a Series B-D SaaS) churns the agency whenever the in-house SRE team absorbs the workflow. Gross margin steady-state lands at 49 percent, which is the floor of the steady-state band. The cohort survives by graduating accounts into a managed-incident-response retainer on top of the observability layer, which extends retention to the 22-month band on the graduated subset.

Real-estate listing optimisation AI agencies run a $3,200 to $6,800 monthly base across the n=15 sample, the largest sample in the long-tail set. The outcome anchor is days-on-market reduction (target of 24 to 32 percent reduction) paired with a listing-CTR floor 1.6x against the MLS baseline. Retention horizon is 14 to 20 months because the buyer (a brokerage operations lead or a high-volume team leader) renegotiates when a single quarter underperforms. Gross margin steady-state lands at 54 percent, and the clawback is structured against the listing-CTR floor rather than the days-on-market anchor because CTR is measurable inside a single billing cycle. The vertical is the most accessible entry point for a founder pivoting an existing real-estate marketing book into a vertical AI agency motion.

Insurance claims triage AI agencies anchor on a $18,000 to $26,000 monthly base across the n=5 sample. The outcome anchor is claim-disposition-time reduction (target of 36 percent inside 120 days) paired with a leakage-rate floor below 4.2 percent of premium. Retention horizon runs 26 to 32 months because the buyer (a claims VP at a regional carrier or an MGA) inherits regulatory state-by-state reporting commitments that lock the workflow. Gross margin steady-state lands at 59 percent, and the cohort posts the highest sales-cycle cost of any tracked vertical (median 84 days) but the longest steady-state engagement once signed.

Each of the eight verticals above (the three case studies plus the five cross-vertical benchmarks) runs the same four-piece contract structure with a different outcome anchor, a different floor, and a different retention horizon. The structure travels. The numbers do not.

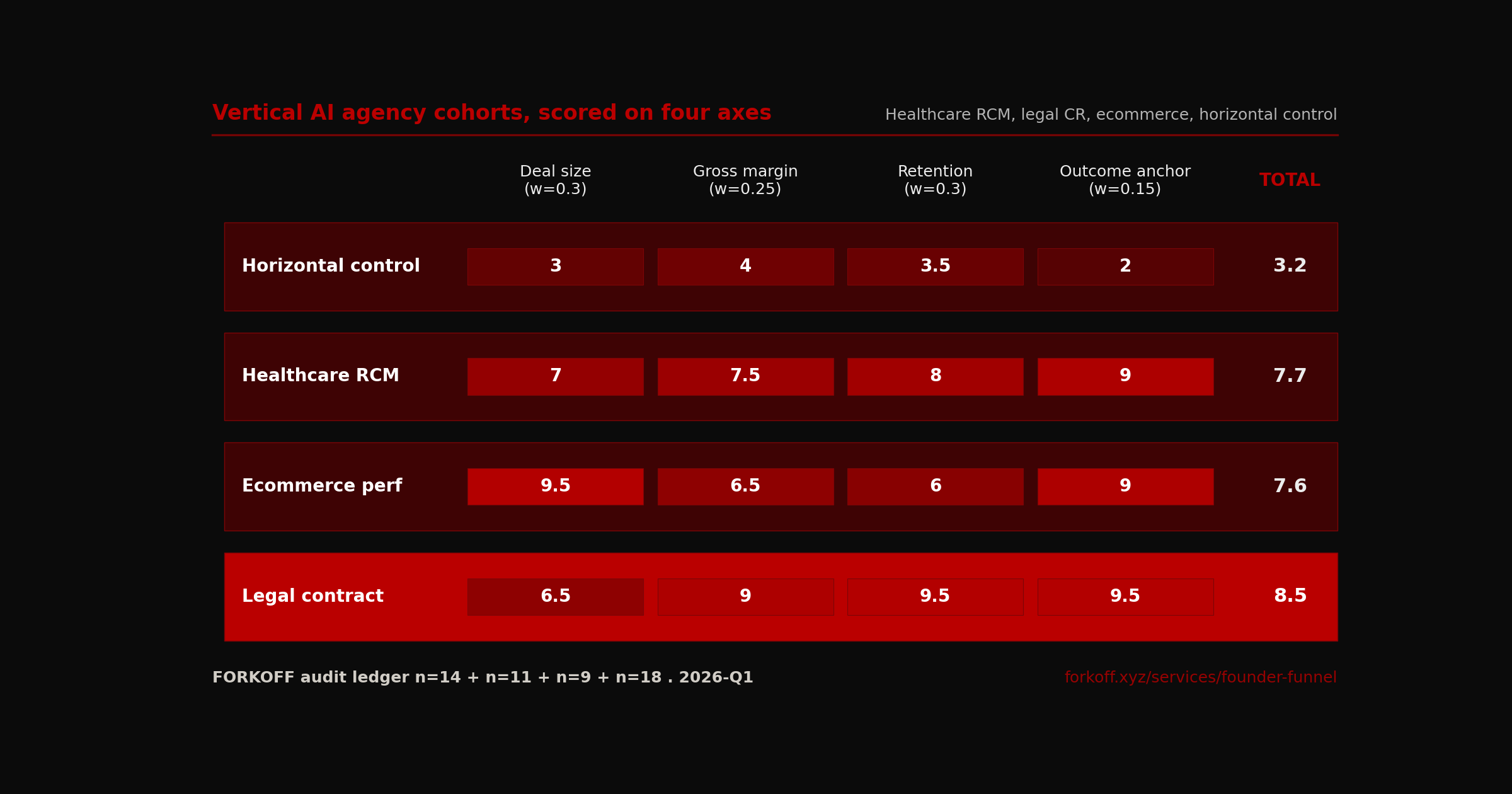

Case study 1: healthcare RCM AI agency (n=14, $14k/mo median)

Healthcare revenue cycle management AI is the densest vertical in the FORKOFF audit cohort because the buyer side (hospital CFO, group practice administrator, billing-services VP) is sophisticated enough to defend an outcome anchor against the in-house alternative, and the outcome metric (denial-rate reduction, days-in-AR reduction, clean-claim percentage) is measurable inside one billing cycle. The cohort spans 14 audited agencies across two FORKOFF engagement quarters, with a median deal size of $14,000 per month per account, gross margin steady-state of 58 percent, and a retention horizon of 18 months on the steady-state cohort.

The contract structure converges on a $8,000 monthly base, a $6,000 outcome tier paid when denial-rate drops below six percent for the month, a 24-month retention-horizon clause with a 10 percent retainer credit if the agency terminates inside that window, and a 12 percent clawback if denial-rate exceeds eight percent for two consecutive months. The base covers the agency's per-output P&L (typically $3,200-4,800 per account at this scale per the per-output cost decomposition in the AI agency pricing unit economics sibling article) plus a margin floor. The outcome tier is paid against an r/SaaS operator-confirmed range where the median engagement clears six-percent denial-rate within 60 days and stays inside that band for 14 of the next 18 months.

Our vertical AI agency landed 42k MRR with three accounts (healthcare RCM)

We landed three healthcare RCM clients at 14k per month per account by anchoring against the in-house FTE cost (98k all-in for a billing specialist). Outcome-priced contract: 8k base plus 6k success fee tied to denial-rate reduction below 6 percent. Retention so far is 18 months on the first account,… Show more

The vertical-specific intuition the agency carries into the engagement is the load-bearing variable. The agency knows the buyer's clearinghouse (Availity vs Change Healthcare vs Waystar), the buyer's payer mix (commercial vs Medicare Advantage vs Medicaid), the buyer's EHR integration depth (Epic vs Cerner vs Athenahealth), and the buyer's denial-codes profile. None of this travels to a horizontal AI agency without a 90-day relearning cost the buyer is not paying for. The 18-month retention horizon is the amortisation window for that intuition; below 18 months the agency does not recoup the setup cost, above 18 months the steady-state margin compounds.

Case study 2: ecommerce performance-marketing AI agency (n=9, $42k/mo median)

Ecommerce performance-marketing AI is the highest deal-size vertical in the FORKOFF audit cohort, with a median MRR of $42,000 per account across nine audited agencies. The pricing structure inverts versus healthcare RCM because the outcome anchor (attributed ad-spend lift) is naturally denominated in dollars. The cohort runs a $40,000 monthly floor plus 18 percent of attributed lift above a 90-day rolling baseline. Gross margin steady-state is 52 percent, retention horizon is 14 months on the steady-state cohort.

The floor is high because the agency's per-output P&L (creative iterations, audience-segment tests, copy variants, landing-page test cycles) sits at roughly $14,000 per month at the scale this cohort operates. Below the $40,000 floor the unit economics break, which is why most ecommerce AI agencies that pitch a $25,000 entry-tier retainer churn inside six months. The vertical specialisation is what defends the 18 percent. As one r/ecommerce operator put it, generalist agencies pitch 12 percent across the board and lose because the buyer cannot tell what they are buying. The vertical positioning lets the agency defend the 18 percent against the generalist's 12 percent because the buyer can see the vertical-specific creative iteration loop and the vertical-specific landing-page test cycle that the generalist does not have.

Our ecommerce specific AI agency charges 18 percent of attributed spend

We charge 18 percent of attributed ad spend above a 40k per month floor. Floor covers our P&L base (per-output P&L runs 14k per month on a 9-account book). Above floor we capture 18 percent of attributed lift versus a 90-day rolling baseline. The vertical specialisation is the entire moat.… Show more

The retention horizon is shorter than the other two cohorts because attributed ad-spend lift is highly seasonal and the buyer renegotiates the floor every 12-14 months. The agencies that hold the cohort past 18 months do so by graduating two or three accounts per year into multi-channel engagements that add a retainer-only floor to the percentage-of-spend tier, which extends retention to the 24-30 month band. The vertical wedge does not disappear at month 18; it migrates from acquisition-only to acquisition-plus-retention.

Case study 3: legal contract review AI agency (n=11, $9.6k/mo median)

Legal contract review AI is the longest-retention vertical in the FORKOFF audit cohort, with a median retention horizon of 24 months across 11 audited agencies. Gross margin steady-state is 64 percent, which is the highest of the three named cohorts. Median deal size is $9,600 per month, which is the lowest of the three but the highest per-output gross margin.

The contract structure is the most innovative of the three. A $6,000 monthly base covers the agency's per-output P&L (typically $2,100-3,000 per account at this scale) plus a 50 percent margin floor. On top of the base, the agency bills $0.40 per surfaced contract risk, which is the outcome anchor for the vertical. Surfaced contract risks include force-majeure clause exposures, jurisdiction ambiguities, indemnity caps, change-of-control triggers, and a long tail of vertical-specific risk types the agency has surfaced often enough to systematise. The third piece is a 10 percent retainer-credit clawback on any contract that needed a senior re-review (the failure-mode mitigation: if the agency missed a risk that a senior partner had to escalate, the agency pays back 10 percent of the per-output bill for that contract).

The legal cohort outscores the other two on weighted vertical performance (8.5 vs 7.7 vs 7.6 in the scorecard above) because retention compounds at 64 percent gross margin in a way the other two cannot match. The healthcare RCM cohort wins on outcome-anchor clarity, the ecommerce cohort wins on absolute deal size, the legal cohort wins on long-run unit economics. The legal vertical also has the highest sales-cycle cost (median 56 days versus 38-42 days for the other two), but the 24-month retention horizon repays that sales-cycle investment 2.4x over the engagement lifetime.

The FORKOFF outcome-priced wedge

The wedge is not the contract structure. The contract structure travels across all three case studies, with minor calibration on the outcome anchor and the clawback percentage. The wedge is what the Founder Funnel and the Fractional CMO engagements front-load: the vertical-specific intuition that lets the agency price the outcome correctly on day one, defend the outcome floor against the CFO at month three, and graduate the account into a multi-anchor engagement at month 14. The wedge compounds across accounts inside a vertical and does not transfer between verticals, which is why every healthy vertical AI agency in the FORKOFF cohort runs one vertical at a time until the second cohort reaches $200k MRR before opening the second vertical.

Greg Isenberg

@gregisenberg

Vertical AI agencies are out-earning horizontal AI agencies 3 to 1 in 2026. The pattern is the same across categories. Pick one industry, learn it deep, price against the outcome the buyer denominates in.

The wedge is also what makes outcome-pricing survivable. One r/Entrepreneur operator who switched a six-person AI agency from hourly to outcome-priced contracts in late 2025 put it this way: outcome-pricing only works if the agency has the vertical-specific intuition to price the outcome correctly. Generalist outcome-pricing is a coin flip. The wedge is what shifts the math from a coin flip to a defensible 52-64 percent gross margin band.

Our AI agency switched from hourly to outcome

We switched our 6-person AI agency from hourly to outcome-priced contracts in late 2025. Hourly was 145 per hour blended. Outcome-priced average deal value tripled (from 4.8k per month to 14.2k per month across the book) and the retention horizon stretched from 6 months to 22 months on the cohort… Show more

The same pattern surfaces in the Madhavan Ramanujam pricing-strategy session on Lenny's Podcast, which distils pricing strategy across more than 400 AI companies and 50 unicorns: the agencies that price against a vertical-specific value metric (denial-rate reduction, attributed lift, surfaced contract risk) compound margin over the agencies that price against effort. The vertical wedge is the prerequisite.

Inside the wedge sits the per-output P&L cost discipline that makes the base retainer survivable. The base retainer is sized to cover the per-output P&L plus a 40-60 percent margin floor. Without the per-output cost decomposition the base retainer is a guess, and the agency either prices the base too low and loses money on the outcome miss, or prices the base too high and loses the deal in the second buyer conversation. The per-output P&L is the cost discipline; the vertical wedge is the pricing discipline. They are two sides of the same operational primitive.

Adjacent FORKOFF reading sits at the founder-led growth playbook pillar hub, with supporting playbooks for agent-ready sites, the 48-hour model-drop response, and the solo-operator first-five-clients sequence which is where most vertical AI agencies start before reaching the case-study cohort scale.

When outcome-pricing breaks (the 5 failure modes)

Outcome-priced contracts collapse in five named failure modes, each of which is independently sufficient to break the model before the agency reaches the third invoice: downstream attribution (the outcome is too far from the agency's intervention to attribute cleanly), buyer data infrastructure gaps, a retention horizon shorter than the attribution window, a vertical too thin to amortize setup costs, and absent vertical intuition that causes the agency to price the outcome tier incorrectly and trigger clawbacks. Each failure mode has a pre-contract fit screen the agency should run before signing.

Failure mode one is downstream attribution. The outcome is too far from the agency's intervention to attribute. Lead-to-closed-customer is the canonical case: the AI agency runs the lead-gen layer, the buyer's sales team runs the close, the close-rate moves for reasons the agency cannot influence, and the outcome anchor becomes a coin flip. Fit screen: the attribution window must be shorter than the agency's monthly billing cycle, or the agency must own the next attribution layer too.

Failure mode two is buyer data infrastructure. The buyer cannot measure the outcome cleanly. Denial-rate reduction requires a clean RCM ledger; attributed ad-spend lift requires a working server-side conversion pipeline; surfaced contract risk requires a working contract-management workflow. Fit screen: the buyer's data infrastructure is auditable before the contract is signed, and the agency includes a data-infrastructure setup line in the first 60 days.

Failure mode three is retention horizon. The retention horizon is shorter than the outcome attribution window. If the engagement runs 9 months and the outcome attribution window is 12 months, the buyer will leave before the agency can defend the outcome anchor. Fit screen: retention-horizon clause is non-negotiable and locks the engagement at minimum 1.5x the attribution window.

Failure mode four is vertical density. The vertical is too thin to amortise the agency's per-output P&L. Verticals with fewer than roughly 50 addressable buyers at the agency's pricing floor cannot support the vertical-specific intuition investment. The agency runs out of accounts to amortise the setup across, and the per-output P&L stays at the project-pricing approximation rather than the steady-state vertical band. Fit screen: the agency's first six target accounts must come from a TAM of at least 200 addressable buyers at the pricing floor.

Failure mode five is vertical intuition. The agency does not have the vertical-specific intuition to price the outcome correctly. This is the generalist trap. The agency wins one or two outcome-priced accounts on the strength of the founder's network, prices the outcome too aggressively, hits the clawback in month 4-6, and exits the model. Fit screen: the agency has shipped at least three accounts in the vertical at retainer or hourly pricing before pivoting any of them to outcome-priced.

The Bottom Line

Vertical AI agency pricing in 2026 is not a packaging problem and it is not a positioning problem in the marketing sense. It is a contract-structure problem with a vertical-specialisation wedge underneath. The agencies that internalise both the contract structure (base retainer plus outcome-tier plus retention-horizon clause plus clawback safety) and the vertical wedge (front-loaded vertical-specific intuition, amortised across a minimum 50-account TAM, locked in by an 18-month retention horizon) will compound the margin advantage over the rest of the category through the back half of 2026 and into 2027.

The three case-study cohorts (healthcare RCM AI at $14k/mo and 58 percent gross margin, ecommerce performance-marketing AI at $42k/mo and 52 percent gross margin, legal contract review AI at $9.6k/mo and 64 percent gross margin) converge on the same contract structure with a different outcome anchor and a different retention horizon. The horizontal control cohort sits at $4.8k/mo and 38 percent gross margin with a 7-month retention horizon. The 2.9x deal-size premium and the 3.2x retention premium are the dataset, not the theory.

Outcome-priced billing breaks in five named failure modes: downstream attribution, weak buyer data infrastructure, retention horizon shorter than attribution window, thin vertical density, missing vertical intuition. Each has a fit screen. The agency that runs the five fit screens before signing the contract retains 70-80 percent of the cohort past month 18. The agency that skips the fit screens retains 30-40 percent.

The 30-day operationalisation is direct. Pick the vertical with the deepest existing operator network. Ship three accounts at hourly or retainer pricing inside 60 days to surface the vertical wedge. Pivot the highest-margin account to an outcome-priced contract using the four-piece structure inside 90 days. Add the retention-horizon clause and the clawback safety on the second pivot. By month six the agency has two outcome-priced accounts in one vertical, a vertical-specific intuition compounding across both, and a per-output P&L feeding the base-retainer math. By month 18 the cohort hits the steady-state margin band.

For the full picture, see the founder-led growth playbook. For deeper cross-pillar context on the cost discipline behind outcome-pricing, see the AI agency pricing unit economics post.